Taxation(UK)

MAIN CONTENT主要内容

A.Explain the operation and scope of the tax systemand the obligations of tax payers and/or their agents and the implications of non-compliance解释税务制度的运作和纳税范围,以及纳税人和其代理人的义务,以及不遵守税法时应承担的责任

B.Explain and compute the income tax liabilities ofindividuals and the effect of national insurance contributions(NIC)onemployees,employers and the self-employed理解并计算个人所得税及国民保险(NIC)对雇员、雇主和自我雇佣者的影响

C.Explain and compute the chargeable gains arising onindividuals理解并计算个人应纳资本利得税

D.Explain and compute the inheritance tax liabilitiesof individuals理解并计算个人的遗产税

E.Explain and compute the corporation tax liabilitiesof individual companies and groups of companies理解并计算单个公司及集团公司的企业所得税

F.Explain and compute the effects of value added taxon incorporated and unincorporated businesses解释并计算增值税对公司和非公司业务的影响

The syllabus大纲

A.The UK tax system and its administration英国的税收制度及其税务管理

1.The overall function and purpose of taxation in amodern economy税收在现代经济中的功能和目的

2.Principal sources of revenue law and practice税收法和惯例的主要来源

3.The systems for self-assessment and the making ofreturns自我报税和纳税申报表系统

4.The time limits for the submission of information,claims and payment of tax,including payments on account提交资料、申报及缴付税款(包括分期付款)的时限

5.The procedures relating to compliance checks,appeals and disputes合规性检查、上诉和争议的有关程序

6.Penalties for non-compliance违反税法的处罚规则

B.Income tax and NIC liabilities所得税和国民保险

1.The scope of income tax所得税的征收范围

2.Income from employment就业收入

3.Income from self-employment个体经营收入

4.Property and investment income投资性房产收入及其他投资收入

5.The comprehensive computation of taxable income andincome tax liability employed and self-employed persons综合计算员工及自雇人士的应纳税额

6.The use of exemptions and reliefs in deferring andminimising income tax liabilities利用减免规则来推迟和减少所得税额

C.Chargeable gains for individuals个人应纳资本利得税

1.The scope of the taxation of capital gains资本利得的征税范围

2.The basic principles of computing gains and losses计算利得和损失的基本原理

3.Gains and losses on the disposal of movable andimmovable property动产和不动产处置的利得和损失

4.Gains and losses on the disposal of shares andsecurities股票和证券买卖的利得和损失

5.The computation of capital gains tax资本利得税的计算

6.The use of exemptions and reliefs in deferring andminimising tax iabilities arising on the disposal of capital assets利用减免规则来推迟和减少因处置资本资产而产生的税务负担

D.Inheritance tax遗产税

1.The basic principles of computing transfers ofvalue计算价值转移的基本原则

2.The liabilities arising on chargeable lifetimetransfers and on the death of an individual因生前资产转移和身故后留下遗产所引发的遗产税

3.The use of exemptions in deferring and minimisinginheritance tax liabilities利用免税来推迟和减少遗产税

4.Payment of inheritance tax缴纳遗产税

E.Corporation tax liabilities企业所得税

1.The scope of corporation tax企业所得税的征收范围

2.Taxable total profits应纳税总利润

3.Chargeable gains for companies企业的应税收益

4.The comprehensive computation of corporation taxliability企业所得税综合计算

5.The effect of a group corporate structure forcorporation tax purposes集团结构对企业所得税的影响

6.The use of exemptions and reliefs in deferring andminimising corporation tax liabilities利用减免规则来推迟纳税和减少公司的税务

F.Value added tax(VAT)增值税(VAT)

1.The VAT registration requirements增值税注册要求

2.The computation of VAT liabilities增值税的计算

3.The effect of special schemes特殊方案的影响

Approach to examining thesyllabus

It will only be possible(for example in June 2019)for candidates to sit TX–UK as a computer based exam(CBE).Paper-based examswill not be run in parallel.

With effect from June 2019,seeded questions havebeen removed from CBE exams and the exam duration is 3 hours for 100 marks.

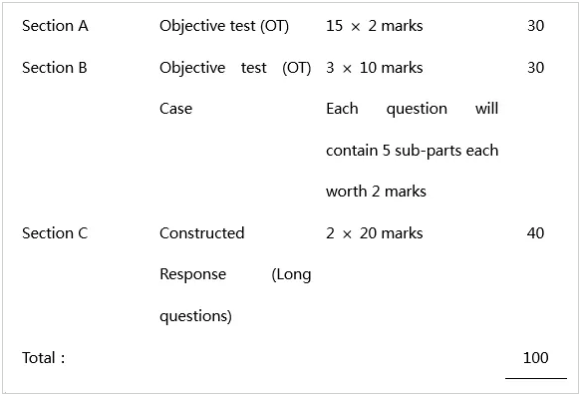

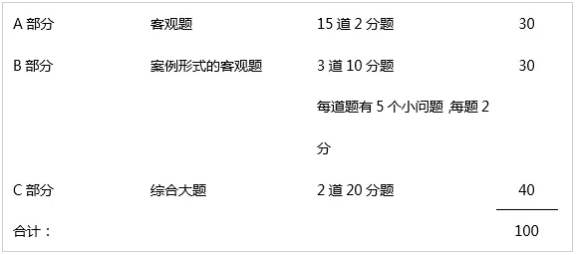

The examination consists of:

考试题型

CBE机考为3小时(外加10分钟阅读考前说明的时间)。

考试结构如下:

acca全科网课还有资料 百度云分享

acca全科网课还有资料 百度云分享 2021年ACCA资料百度云下载,ACCA免费下载

2021年ACCA资料百度云下载,ACCA免费下载 2021年ACCA备考必备资料全套免费下载,ACCA资料免费

2021年ACCA备考必备资料全套免费下载,ACCA资料免费